Aluminium plays a central role in Construction, Automotive, Packaging and Clean

Energy Industries. As the world’s most widely used non-ferrous metal, Aluminium’s

unmatched combination of being lightweight, durable, conductive, and fully recyclable

makes it indispensable.

Highlights Mar 2025 – 2026

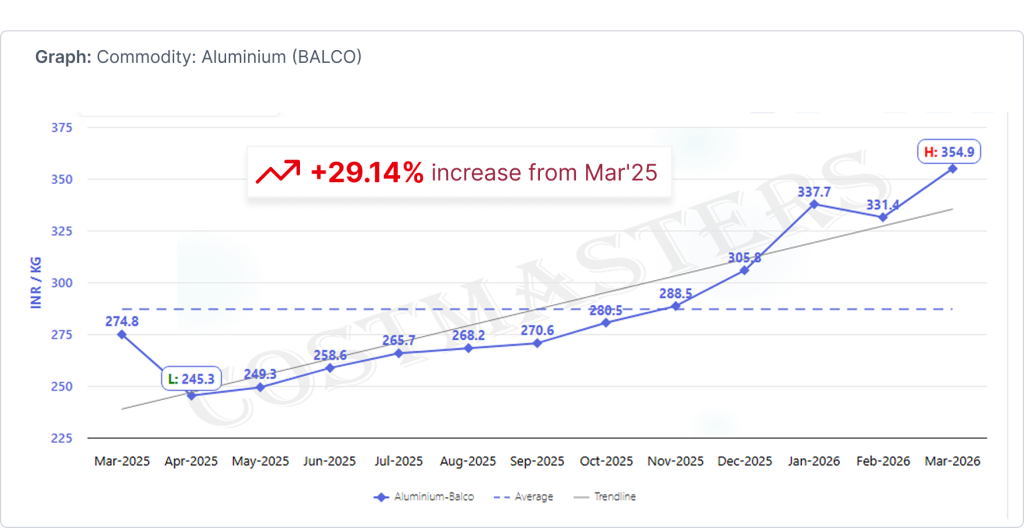

March – April 2025

Aluminium prices fell from to about ₹245/kg as concerns over global economic growth and

new tariffs weighed on industrial metals demand.

July – September 2025

Prices rose from roughly ₹260/kg to about ₹270/kg as global inventories declined and

tightening supply supported the Aluminium market

December 2025 – January 2026

Aluminium increased to about ₹330/kg as low global stockpiles and strong demand from

manufacturing and energy-transition sectors pushed prices higher

January – February 2026

Prices fell around 5% as worries over possible new tariffs and profit-taking pushed metals

lower. The dip was short-lived.By late February, prices were climbing back, driven by

tightening global supply and steady demand from the electric vehicle and clean energy

sectors.

Key Drivers

China’s Production Cap

China enforces a strict government ceiling on primary Aluminium output, leaving virtually no

room to expand supply when prices rise. This acted as a persistent structural constraint

that kept the prices elevated.

Declining Global Inventories

LME warehouse stocks fell steadily through 2025, leaving little metal available to meet

demand. This kept prices firm even when the broader economy weakened.

EV, Solar & Grid Infrastructure Demand

Electric vehicles, solar panels, and power grids all rely heavily on aluminium, and demand

from these sectors kept growing even when the broader economy slowed. This acted as

a safety net for prices, stopping them from falling as steeply as they have in previous

downturns.

US Import Tariffs

Escalating US tariffs on aluminium imports disrupted decades of established global trade

flows and pushed domestic premiums to record highs. Tariff announcements also

periodically triggered broader sentiment-driven sell-offs across metals markets

Geopolitical Supply Disruptions

Conflict in the Middle East suspended gas supplies to major Gulf smelters, forcing

production shutdowns in a region supplying a significant share of global output. Combined

with earlier bauxite and alumina disruptions in Guinea and Australia, geopolitical risk

became a recurring and increasingly impactful price driver

Market Impact

Global

A near 47% price rise over the year made Aluminium significantly more expensive

for industries like automotive, construction, and packaging — sectors that have

no easy substitute for the metal.

US tariffs broke decades of established trade routes, forcing buyers and sellers to

EV, Solar & Grid Infrastructure Demand find new partners and adding cost and delays across global supply chains.

India

Higher global prices helped aluminium producers earn more, but hurt downstream

industries like auto parts, cables, and packaging that depend on aluminium as a

key raw material.

With the US imposing steep tariffs, Indian exporters lost their second-largest

market overnight and had to pivot to Europe and Southeast Asia to find new

buyers.

Forecast and Market Outlook

Market analysis suggest Aluminium prices to remain elevated through 2026, with China’s

production ceiling limiting supply growth while EV, solar and grid demand continues to

expand — keeping the structural floor under prices firm. Any additional disruption in

output from Gulf smelters could push prices to fresh highs, while an easing of tensions

could trigger a sharp pullback from current levels.